And it’s gone!

We are referring to the $300 billion of taxpayer funds that will go down the tubes at the stroke of Joe Biden’s pen upon his impending cancellation of $10,000 of student debt. And in the case of married couples, that covers households with incomes up to $250,000!

The legal claim to justify this action as invoked by the Department of Eduction: it is “a program of categorical debt cancellation directed at addressing the financial harms caused by the COVID-19 pandemic.”

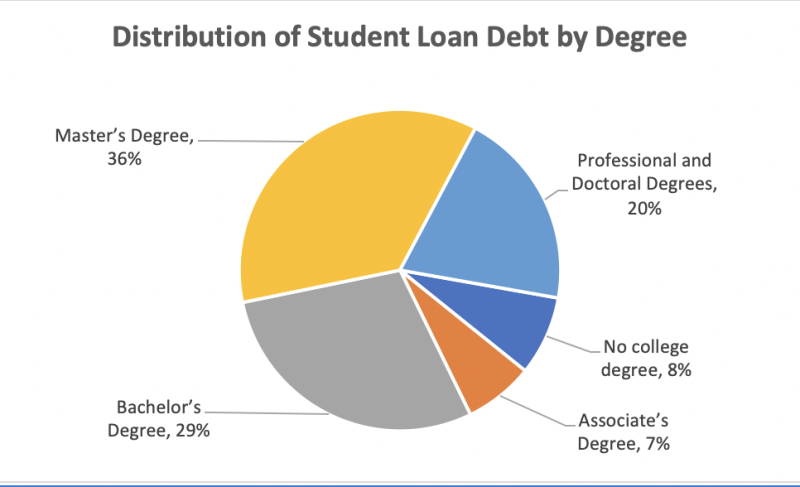

Only 37% of Americans have a 4-year college degree, only 13% have graduate degrees and just 3% have a PhD or similar professional degree. Yet a full 56% of student loan debt is held by people who went to grad school and 20% is owed by the tiny 3% sliver with PhDs.

So Biden’s debt cancellation plan would amount to taking money from a plumber to pay the debt of a lawyer. Here’s the breakdown by degree status of who will get a $10,000 gift from Joe:

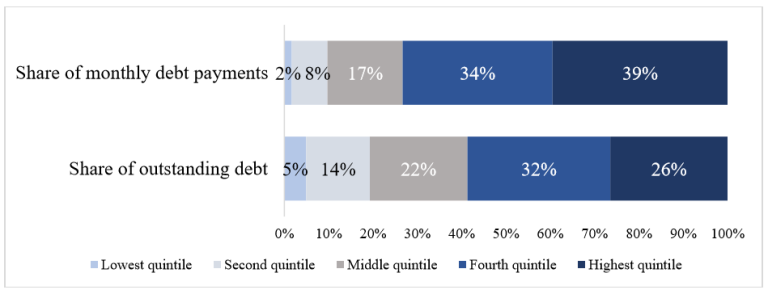

Not surprisingly, student debt outstanding and share of debt repayments (prior to the Covid moratorium, which is still in effect and likely to be extended through year end by Biden) is highly skewed to the upper end of the income ladder.

Thus, the highest-income 40 percent of households (those with incomes above $74,000) owe almost 60 percent of the outstanding education debt and make almost 75% of the payments. By contrast, the lowest-income 40 percent of households hold just under 20 percent of the outstanding debt and make only 10 percent of the payments.

Nor do even these figures capture the full difference in payment burdens. That’s because a growing share of borrowers participate in income-driven repayment (IDR) plans, which do not require any payments from those whose incomes are too low and limit payments to an affordable share of income for others.

As a result, out-of-pocket loan payments (pre-moratorium) are extremely concentrated among high-income households: Fully, 73% of payments in 2019 were accounted for by the top 40% of households.

On the other hand, few low-income households enrolled in IDR are required to make any payments at all, explaining why the bottom 40% of student loan households accounted for just 10% of payments in 2019.

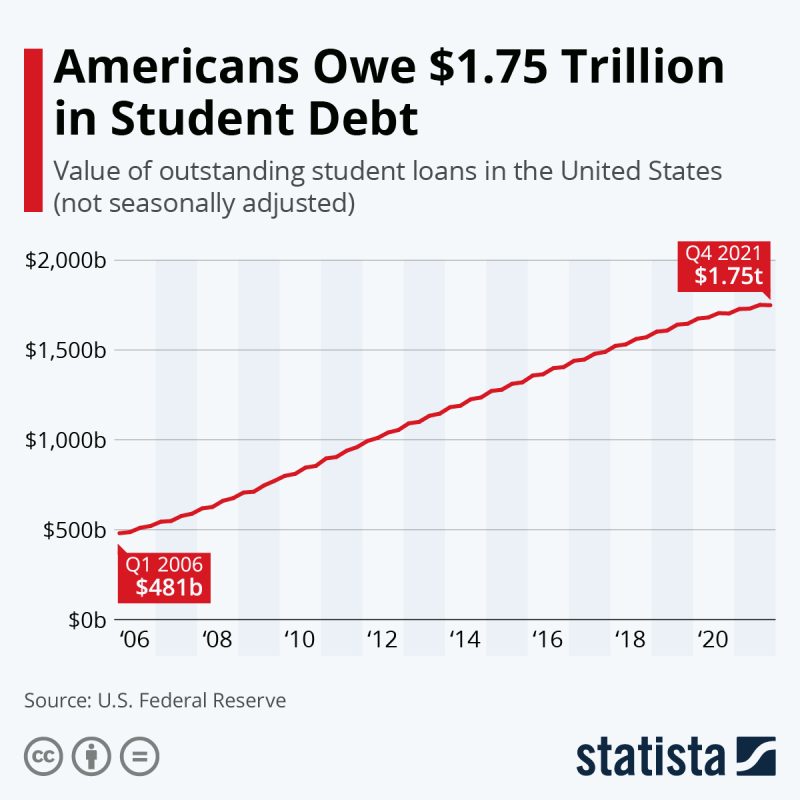

Approximately 43 million student loan borrowers in the United States owe a collective nearly $1.75 trillion in federal and private student loan debt as of August 2022, according to the Federal Reserve Bank of St. Louis. But when you look at the average amounts owed, the case is crystal clear: Student debt is overwhelmingly an investment in professional credentialization that should never have been an obligation of the taxpayers in the first place.

And now between subsidized interest rates, the Covid moratoriums and Joe Biden’s $10,000 cancellation, it amounts to a taxpayer subsidy of the most affluent class of American citizens.

While the average U.S. household with student debt owes $58,957, according to NerdWallet’s 2021 household debt study, here is the breakdown by degree earned:

| Debt type | Average debt |

|---|---|

| Bachelor’s degree debt | $28,950 |

| Graduate school loan debt | $71,000 |

| Parent PLUS loan debt | $28,778 |

| Law school debt | $145,500 |

| MBA student debt | $66,300 |

| Medical school debt | $201,490 |

| Dental school debt | $292,169 |

| Pharmacy school loan debt | $179,514 |

| Nursing school student debt | $19,928: Associate Degree Nursing (ADN) $23,711: Bachelor of Science in Nursing (BSN)$47,321: Master of Science in Nursing (MSN) |

| Veterinary school debt | $183,302 |

So the question recurs. What’s up with this absurd plan to redistribute income to the tippy-top of the economic and social ladder?

You could answer that query with “November 8th 2022” and be done with it, but that wouldn’t actually get to the bottom of the matter.

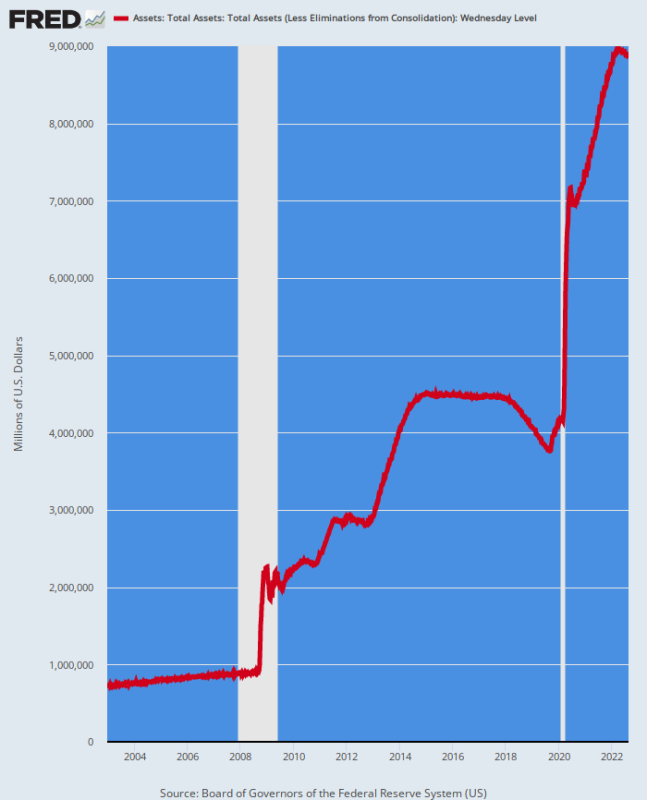

The truth is, after $6 trillion of Covid stimmies—most of which were monetized by the Fed—there is no fiscal standards left in Washington at all. And Donald Trump and the GOP were every bit as culpable as Biden.

Indeed, Biden’s pending $300 billion student debt giveaway is a piker compared to the massive debt cancellations under the GOP’s PPP loans (payroll protection plan).

More than 11.8 million Paycheck Protection Program (PPP) loans were issued as of June 30, 2021, with 708 borrowers receiving the maximum loan amount of $10 million.

Yet of that massive outpouring of “loans,” the Small Business Administration (SBA) data shows that about 94% of PPP loans that were approved in 2020 had been forgiven as of December 2021!

Overall, only $28 billion of all PPP loans, which totalled upwards of $800 billion, remained unforgiven as of February 2022, a recent Bloomberg News analysis suggested. And as of April 2022, the average dollar amount forgiven was $95,700.

In short, the bipartisan duopoly is in the free stuff business in a manner that wasn’t even imaginable two decades ago. Joe Biden is just the latest politician to jump on the bandwagon—-an outbreak of fiscal incontinence that has far less to do with the inherent spending propensity of democratic politicians than it does with the money-printing madness of the unelected central bankers who actually run the nation’s financial affairs.

Fed Balance Sheet, 2002-2022

Republished from David Stockman’s Corner

Join the conversation:

Published under a Creative Commons Attribution 4.0 International License

For reprints, please set the canonical link back to the original Brownstone Institute Article and Author.