In case you’ve still got money in a bank, Bloomberg is warning that defaults in commercial real estate loans could “topple” hundreds of US banks.

Leaving taxpayers on the hook for trillions in losses.

The note, by Senior Editor James Crombie, walks us through the festering hellscape that is commercial real estate.

To set the mood, a new study predicts that nearly half of downtown Pittsburgh office space could be vacant in 4 years. Major cities like San Francisco are already sporting zombie-apocalypse downtowns, with abandoned office buildings baking in the sun.

So what happened?

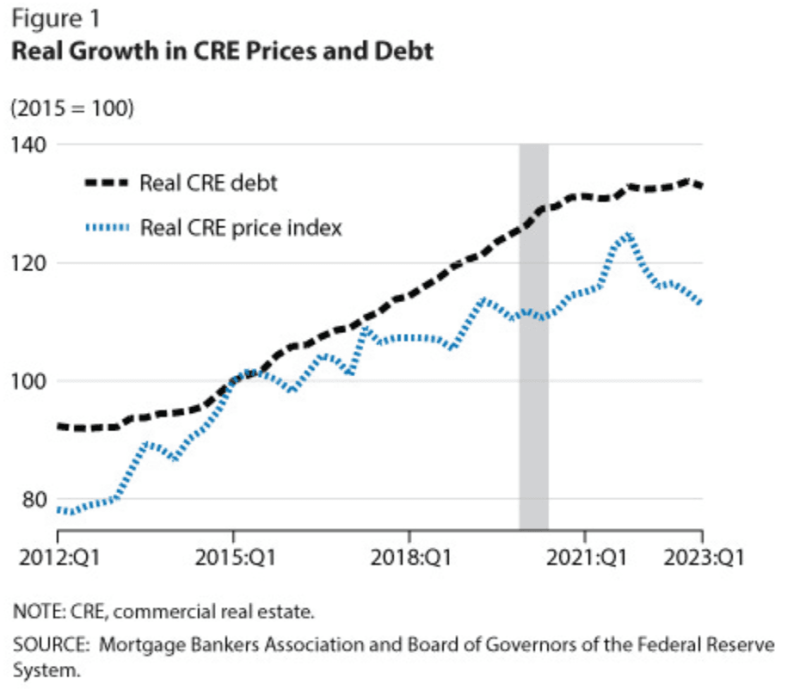

The Fed’s yo-yo interest rates first flooded real estate with low rates and cheap money. Which were overbuilt.

Then came the lockdowns, which forced millions to figure out new workday patterns. People liked foregoing the long commute (not to mention the free money). Despite every effort, downtown businesses have not been able to get all workers back.

These days, everyone talks about hybrid models of working, some in-person and some remote. But judging from observation, remote is winning. In any case, even a 30 percent reduction in the footprint of office space once the leases are renewed could topple the entire sector.

The restaurant and retail sectors of downtown feel the pinch, with more closures all the time. Adding to the pressure are absurd levels of inflation and ever-riskier streets on matters of personal security. Put it all together and there is ever less reason to slog to the office.

When the Fed panic-hiked interest rates in the 2021 inflation, that put trillions of commercial real estate underwater even without other factors. Add to that crime, inflation, plus remote work, and you have a dangerous mix that could toppled cities as we know them.

This could mimic and elaborate upon last year’s bank crisis, where falling bond prices panicked depositors. That crisis only stopped when Treasury Secretary Janet Yellen and Fed Chairman Jerome Powell effectively bailed out every bank in America with sweetheart loans written on fictitious asset values along with unlimited taxpayer guarantees through the comically underfunded FDIC.

By the way, the FDIC is essentially guaranteeing over $20 trillion in deposits on just over $100 billion. So they’ve got a half-penny on the dollar.

Without those government pre-bailouts, one paper last year by researchers at Stanford and Columbia estimated that 1,619 US banks – about a third of them – could be at risk of failure.

The problem is that nothing was actually fixed. In fact, it’s getting worse. For the simple reason that as the months roll by there’s more and more debt coming due.

And that brings us to Crombie, who notes that there’s $929 billion of commercial real estate debt coming due in the next 9 and a half months.

That’s up 28% from last year, and it’s getting bigger every day as banks pretend loans are still healthy by effectively adding missed payments.

We’re starting to see glitches in the matrix; New York Community Bank just went through a near-death experience over its garbage portfolio of commercial real estate loans, dropping almost 80% before it was bailed out by vulture investors while the megabanks hover like megavultures.

More will come. Potentially a lot more: a recent study from the National Bureau of Economic Research estimated that up to 385 American banks could fail over commercial real estate loans alone.

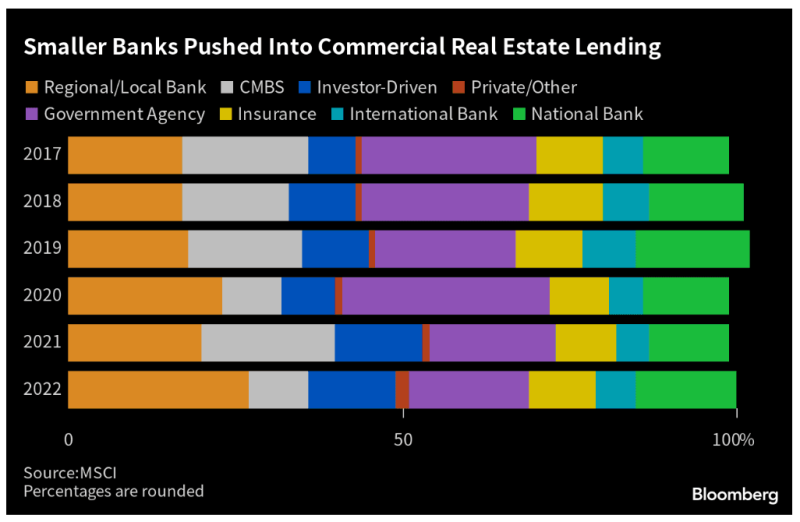

These would overwhelmingly be small regional banks, who typically hold a third of their assets in commercial real estate loans.

They hold so much because they know their local markets best, but the Fed poisoned that chalice by flooding easy money to developers.

For now we’re only seeing the sickest banks dropping out of the herd. That could dramatically accelerate as that $1 trillion plus in loans come due.

Commercial real estate delinquency rates have already jumped to 6 and a half percent – up 30% in a matter of months. Rates of distress in office loans just hit 11%.

When the smoke clears, we could lose dozens, even hundreds, of regional banks. Going by the last time with savings and loans, taxpayers ate 80% of the losses.

Meaning you could be on the hook for trillions, while the megabanks gorge on the carcass.

Slashing interest rates could staunch the bleeding. But with inflation marching up every month – currently at 5 and a half percent annualized – that’s not going to happen.

This article draws from a piece posted on Substack

Join the Conversation

Published under a Creative Commons Attribution 4.0 International License

For reprints, please set the canonical link back to the original Brownstone Institute Article and Author.