The recent controversies embroiling many corporations, notably Target, Disney, and Imbev (the owner of Anheuser-Busch) has brought the issue of stakeholder “capitalism”* to the center of American political discourse. These controversies demonstrate clearly why corporations and their executives should not indulge their own preferences or preferences of “stakeholders” other than shareholders, but should instead limit their efforts to what is already a very demanding task–maximizing shareholder value.

At its root, stakeholder capitalism represents a rejection–and usually an explicit one–of shareholder wealth maximization as the sole objective and duty of a corporation’s management. Instead, managers are empowered and encouraged to pursue a variety of agendas that do not promote and are usually inimical to maximizing value to shareholders. These agendas are usually broadly social in nature intended to benefit various non-shareholder groups, some of which may be very narrow (transsexuals) or others which may be all encompassing (all inhabitants of planet earth, human and non-human).

This system, such as it is, founders on two very fundamental problems: the Knowledge Problem and agency problems.

The Knowledge Problem is that no single agent possesses the information required to achieve any goal–even if universally accepted. For example, even if reducing the risk of global temperature increases was broadly agreed upon as a goal, the information required to determine how to do so efficiently is vast as to be unknowable. What are the benefits of a reduction in global temperature by X degrees?

The whole panic about global warming stems from its alleged impact on every aspect of life on earth–who can possibly understand anything so complex? And there are trade-offs: reducing temperature involves cost. The cost varies by the mix of measures adopted–the number of components of the mix is also vast, and evaluating costs is again beyond the capabilities of any human, no matter how smart, how informed, and how lavishly equipped with computational power. (Daron Acemoğlu, take heed).

So what do climate-concerned executives do? Adopt simplistic goals–Net zero! Adopt simplistic solutions–deprive fossil fuel companies of capital!

Maximizing shareholder value is informationally taxing enough as it is. Pursuing “social justice” and saving the planet is vastly, vastly more so.

Meaning that even if corporate executives were benevolent–a dubious proposition, but put that aside for now–they would no more possess the information necessary to pursue their benevolence than does a benevolent social planner.

Instead, executives pursuing non-shareholder wealth objectives are almost certain to be Sorcerer’s Apprentices, believing they are doing right but creating havoc instead.

Agency problems exist when due to information asymmetries or other considerations, agents may act in their own interests and to the detriment of the interests of their principals. In a simple example, the owner of a QuickieMart may not be able to monitor whether his late-shift employee is sufficiently diligent in preventing shoplifting, or exerts appropriate effort in cleaning the restrooms and so on.

In the corporate world, the agency problem is one of incentives. The executives of a corporation with myriad shareholders may have considerable freedom to pursue their own interests using the shareholders’ money because any individual shareholder has little incentive to monitor and police the manager: other shareholders benefit from, and thus can free ride on, any individual’s efforts. So managers can, and often do, get away with extravagant waste of the resources owned by others placed in their control.

This agency problem is one of the costs of public corporations with diffuse ownership: this form of organization survives because the benefits of diversification (i.e., better allocation of risk) outweigh these costs. But agency costs exist, and increasing the scope of managerial discretion to, say, saving the world or achieving social justice inevitably increases these costs: with such increased scope, executives have more ways to waste shareholder wealth–and may even get rewarded for it through, say, glowing publicity and other non-pecuniary rewards (like ego gratification–“Look! I’m saving the world! Aren’t I wonderful?”)

Indeed, we now have a highly leveraged agency problem, due to the ability of asset managers like BlackRock to vote the shares of their customers, thereby allowing the likes of Larry Fink to force not just one corporation to indulge his preferences, but hundreds if not thousands. Fink and his ilk can influence the direction of sums of capital dwarfing anything in history to pursue their agendas.

The agency problem pervades stakeholder capitalism even when you dispense with the idea that the shareholders are the principals, and expand the set of principals to include non-shareholder interests (which is inherently what “stakeholder” capitalism means). And as discussed above, in stakeholder capitalism these interests conceivably encompass all life on earth.

The problem is that just as shareholders are diffuse and cannot prevent managers from acting in their interest, stakeholders are often diffuse too. And in the case of climate, All Life On Earth is about as diffuse as you can get. Furthermore, whereas at least in principle shareholders can largely agree that the firm should maximize their wealth, when one expands the set of interests, these interests will inevitably conflict.

So what happens? Just as in politics and regulation, small, cohesive minority groups which can organize at low cost will exert vastly disproportionate influence. It is not surprising, therefore, that companies like Target (to name just one) have responded to the interests of transsexuals–a decidedly narrow minority group–and given the finger to others who should be “stakeholders” as well, namely customers. Customers being a diffuse, dispersed, heterogeneous group that is costly to organize–precisely for the same reasons that it is costly for shareholders to organize.

(The Target and Bud Light episodes suggest that social media has reduced the costs of organizing diffuse groups, but even so, it is far costlier to do that than to organize ideological minorities.)

In other words, stakeholder capitalism inevitably creates a tyranny of minorities, and especially highly ideological minorities (because a shared ideology reduces the cost of organizing). Minority stakeholders will succeed in expropriating majority ones.

Minority tyranny is the big problem with democratic politics. Extending it to vast swathes of economic life is a nightmare.

So what is stakeholder capitalism, when you get down to it? A world of Sorcerer’s Apprentice executives (the Knowledge Problem) with bad incentives (the agency problem).

Other than that, it’s great!

Some libertarians have a peculiar take on this phenomenon. They view stakeholder capitalism as benign, because it is undertaken by private actors, rather than the government.

This take is gravely mistaken. It ignores fundamental principle, and commits at least two category errors.

The forgotten principle is that a liberal society should aim to minimize coercion.

The first category error is to believe that private actors cannot coerce–only governments can. In fact, private actors–including corporations and their managements–can clearly coerce. Come and see the violence inherent in the stakeholder capitalism system straight from the mouth of its primary exponent:

“We are forcing behaviors.” Coercive enough for you? Help, help, I’m being repressed:

That bit, by the way, concisely expresses the stakeholder capitalism movement, right down to the “Shut up!” and “You bloody peasant!”

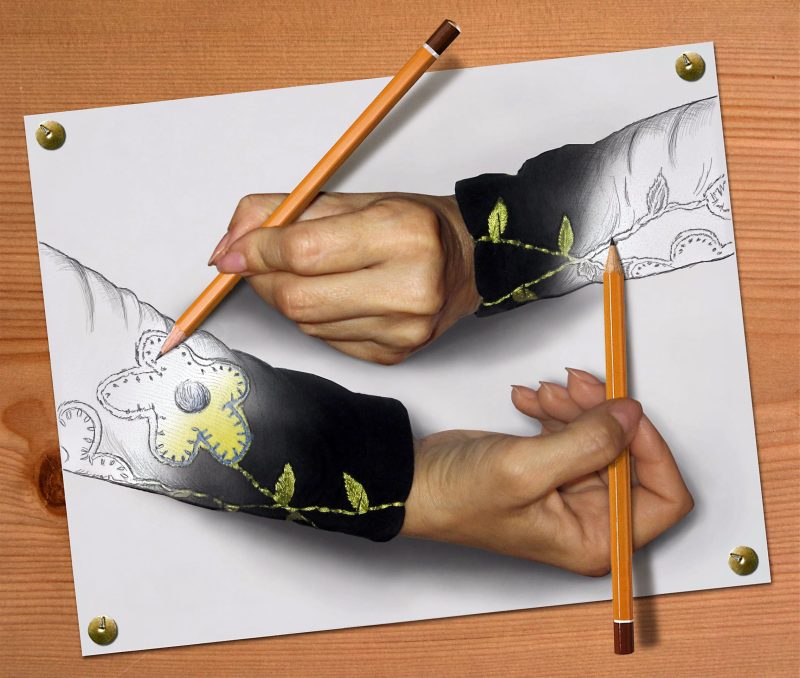

The second category error is to believe that there is some sort of clear boundary between private entities (corporations especially) and governments. In fact, the true picture is like the Escher Hands:

Corporations influence government. Government influences corporations (cf., Twitter Files, etc.–the examples are almost endless). Governments often outsource coercion to corporations. Corporations induce the government to coerce for their benefit–and to the detriment of alleged “stakeholders” like customers, labor, and competitors.

Furthermore, as Arrow’s impossibility theorem teaches, any coherent social welfare function (i.e., any theory of social justice) is inherently dictatorial, and thus inherently coercive. Thus, to the extent that stakeholder capitalism is intended to implement any particular vision of social justice, it is necessarily dictatorial, and hence coercive. It is antithetical to a liberal system like that envisioned by Hayek; that is, one in which a set of general rules is established under which people can pursue their own, inevitably conflicting, aspirations. (Less formally than Arrow, Hayek also argued that any system of social justice is inherently coercive and dictatorial.)

Stakeholder capitalism is therefore a truly malign movement, and an anathema to liberal principles. We need to drive a stake through its heart, before it stakes us to the ant hill.

*I put “capitalism” in quotes because stakeholder capitalism is an oxymoron. Recall that capitalism is an epithet devised by Marx to describe a system ruled in the interests of capital, i.e., shareholders. Stakeholder capitalism is a system intended to be ruled in the interest of everyone but capital. Hence the oxymoron.

** Jeffrey Tucker has also eloquently and rightly excoriated the response of many libertarians to COVID. Here again, these libertarians forgot that limiting coercion is the bedrock libertarian principle.

Reposted from the author’s site.

Join the Conversation

Published under a Creative Commons Attribution 4.0 International License

For reprints, please set the canonical link back to the original Brownstone Institute Article and Author.